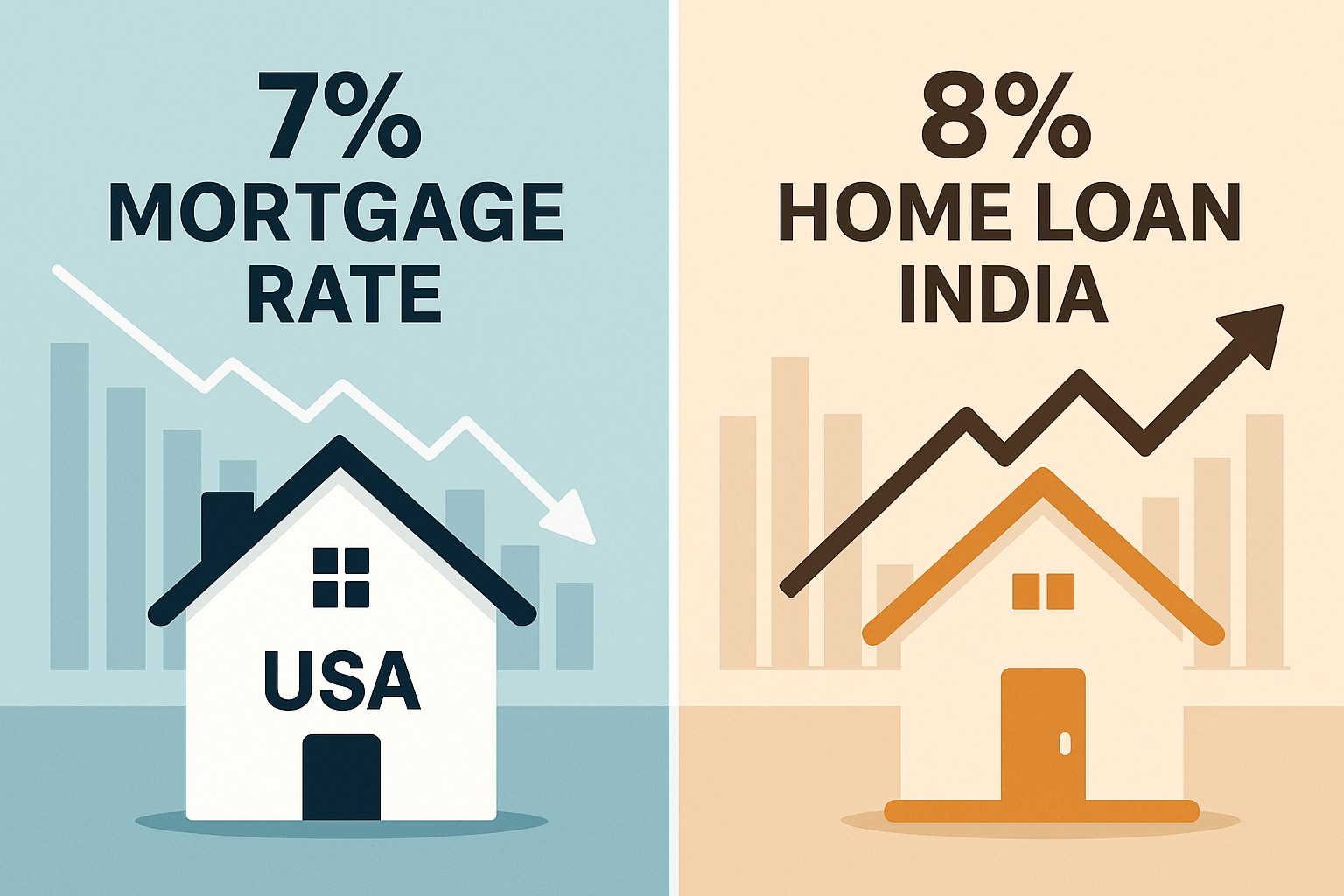

Mortgage rates are once again in the spotlight—this time for two very different reasons across the globe. In the United States, interest rates for home loans are inching closer to the 7% threshold, causing concern among borrowers and real estate stakeholders. Meanwhile, in India, mortgage rates have begun to decline, driven by a recent 25 bps repo rate cut by the Reserve Bank of India (RBI).

With housing affordability becoming a global concern and real estate markets adjusting to shifting interest rate cycles, the trends in mortgage rates are critical indicators of economic health, consumer confidence, and policy direction.

Let’s dive into what’s driving these divergent mortgage movements and what they mean for borrowers, investors, and policymakers.

1. U.S. Mortgage Rates – Hovering Near 7% Again

As of May 19, 2025, average mortgage rates in the United States remain elevated, though slightly down from late 2024 levels. Despite expectations that the Federal Reserve may begin rate cuts later this year, rates have remained sticky due to inflation concerns and strong labor market data.

Current U.S. Mortgage Rates (as of May 19, 2025)

| Loan Type | Average Interest Rate |

|---|---|

| 30-Year Fixed | 6.90% – 7.05% |

| 15-Year Fixed | 6.08% – 6.31% |

| 7/1 ARM | ~6.49% |

(Source: Freddie Mac PMMS)

These figures mark a notable change from the sub-3% mortgage rate environment seen just a few years ago during the pandemic stimulus era. The persistent high-rate regime is affecting:

- First-time homebuyers, who are facing the double whammy of elevated home prices and expensive financing.

- Real estate developers, who are seeing reduced demand in both residential and commercial segments.

- Homebuilders, who are slowing new construction amid concerns of unsold inventory.

What’s Driving U.S. Rates Higher?

- Inflationary Pressure: Despite Fed efforts, core inflation has not yet returned to the 2% target.

- Sticky Fed Policy: The Federal Reserve has signaled that any interest rate cuts will be data-dependent and delayed.

- Bond Market Volatility: Mortgage rates are largely influenced by the 10-year Treasury yield, which remains elevated amid global macro uncertainty.

2. India Mortgage Rates – Falling Below 8%

In contrast, the Indian home loan market is witnessing easing rates, thanks to a proactive monetary policy shift by the RBI, which cut the repo rate by 25 basis points in April 2025.

This is the first rate cut by the Indian central bank since early 2023, and it comes on the back of moderating inflation, strong forex reserves, and a need to boost consumption ahead of the festive season.

Current Home Loan Interest Rates in India (May 2025)

| Bank | Starting Interest Rate (p.a.) |

|---|---|

| State Bank of India (SBI) | 8.00% |

| HDFC Bank | 8.50% |

| ICICI Bank | 8.75% |

| Axis Bank | 8.75% |

(Source: Moneycontrol, SBI, HDFC, ICICI Bank websites)

These rates are variable and linked to the external benchmark rate (EBLR), which is now reflecting the RBI’s accommodative policy stance.

Why Are Indian Rates Falling?

- RBI Policy Easing: A 25 bps cut in repo rate to 6.00% has started to reflect in bank lending rates.

- Improved Liquidity: Banks have more lending capacity due to strong deposit growth and stable NPA levels.

- Real Estate Push: Government schemes like PMAY and increasing urbanization have increased the push for affordable housing finance.

3. Comparison: U.S. vs. India Mortgage Trends

| Factor | United States | India |

|---|---|---|

| Central Bank Policy | Hawkish (no cuts yet) | Dovish (25 bps cut in April) |

| Avg. Mortgage Rate | ~7% (30-year fixed) | 8.00% – 8.75% (floating) |

| Housing Affordability | Declining | Improving (in select cities) |

| Rate Trend | Flat to Up | Downward |

| Key Driver | Inflation, Fed Policy | Liquidity, Real Estate Push |

4. Implications for Borrowers

In the U.S.:

- Refinancing remains unattractive, unless loans were originated during the ultra-low rate period.

- Adjustable-rate mortgages (ARMs) are regaining popularity but carry reset risks.

- New homebuyers may need to buy down rates using points or negotiate better terms via FHA loans.

In India:

- Borrowers can expect lower EMIs if their loans are linked to floating rates.

- Balance transfers are gaining momentum as borrowers move to lenders offering better rates.

- Fixed-rate loans are still less popular due to high spreads compared to floating options.

5. Real Estate Market Impact

U.S. Real Estate Trends:

- Home sales are down ~20% YoY due to financing constraints.

- Inventory levels remain low, especially for affordable homes.

- New construction is slowing despite housing shortages in metro markets.

India Real Estate Trends:

- Affordable and mid-segment housing demand is picking up.

- Tier-2 and Tier-3 cities are leading the growth, driven by lower prices and better credit access.

- Developers are offering no EMI till possession schemes to attract buyers.

6. Expert Outlook

United States

Analysts at Wells Fargo and Goldman Sachs predict that 30-year mortgage rates may stabilize around 6.75% by late 2025, provided the Fed initiates cuts by Q3.

However, if inflation persists, mortgage rates could stay higher for longer, delaying housing recovery.

India

Market experts believe that banks will likely cut home loan rates further by 25–50 bps if the RBI maintains a dovish stance. Real estate in cities like Hyderabad, Pune, and Ahmedabad is expected to benefit the most from rate transmission.

Conclusion

The global mortgage market is diverging in 2025—tight in the U.S., but loosening in India. For prospective borrowers and real estate investors, understanding these macro trends can help make more informed financial decisions.

- In the U.S., patience may be key as rates slowly normalize.

- In India, this could be the right window to lock in lower rates, especially if you’re considering a home purchase or refinance.

Whether you’re a borrower, a banker, or an investor, staying updated on mortgage movements is essential for navigating today’s complex economic environment.

Disclaimer

This article is for informational purposes only and does not constitute financial advice. Mortgage rates are subject to market fluctuations. Always consult your bank or financial advisor before taking a loan or investment decision.